SMM reported on July 3:

At the beginning of June, driven by policy-related news, upstream suppliers significantly raised their quotes for Pr-Nd products. However, downstream demand failed to keep pace, and due to reluctance to accept high prices, Pr-Nd prices began to correct in mid-June. Nevertheless, in late June, influenced by factors such as long-term agreement deliveries at month-end, frequent tenders by large magnetic material manufacturers, and procurement by leading northern manufacturers, upstream suppliers' confidence strengthened, quotes became firmer, and Pr-Nd prices stabilized accordingly. During the same period, dysprosium and terbium prices generally remained in the doldrums.

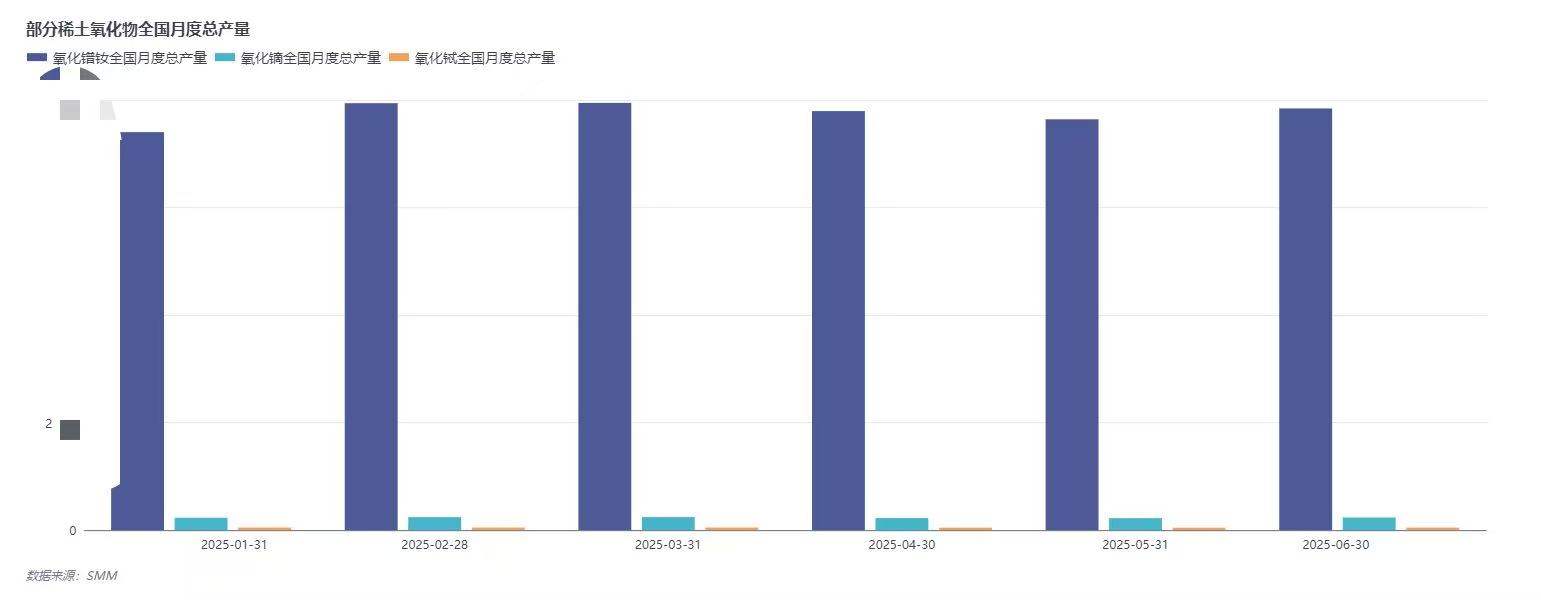

Overall, rare earth market prices in June mostly fluctuated rangebound, with production increasing MoM: Pr-Nd oxide rose by 1.48%, dysprosium oxide fell by 0.31%, and terbium oxide dropped by 1.6%. Production of both light rare earths and medium-heavy rare earths increased MoM. Entering July, the rare earth market has remained stable overall.

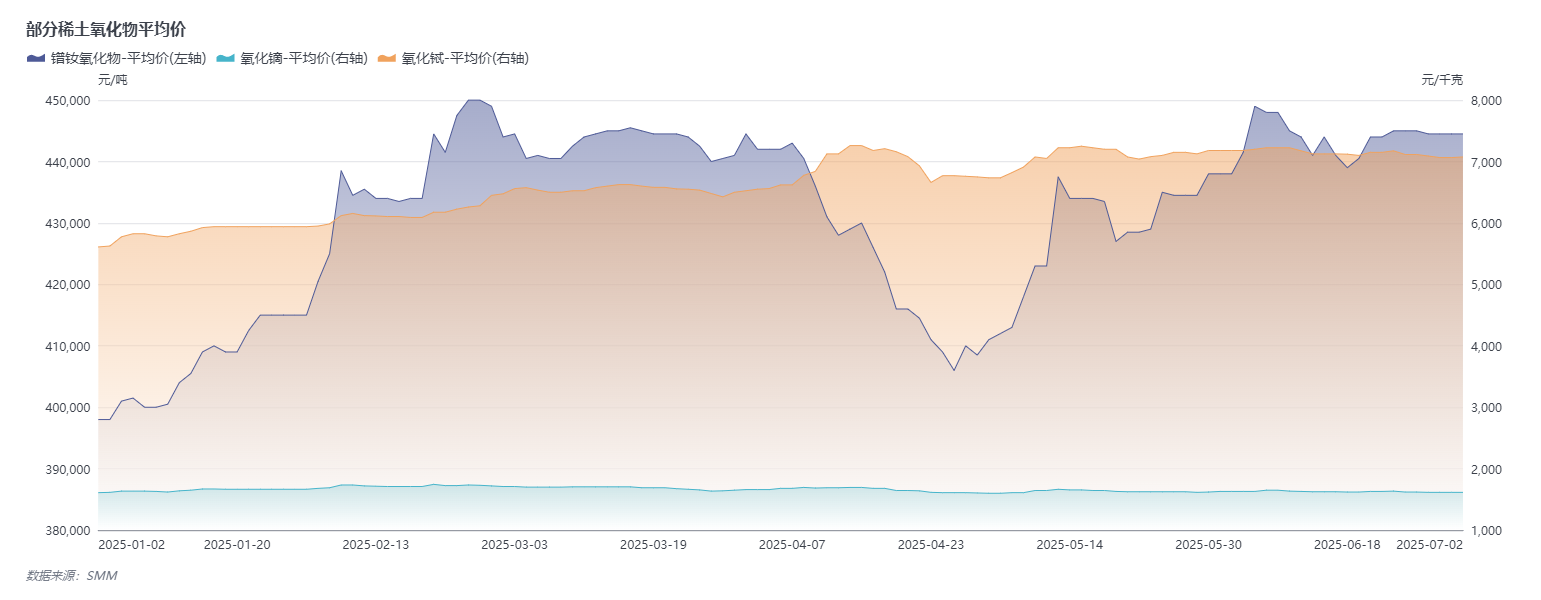

Pr-Nd oxide rose by 1.48% in June, while dysprosium oxide and terbium oxide fell slightly.

》Click to view SMM rare earth spot prices

》Subscribe to view historical price trends of SMM metal spot prices

Regarding light rare earth prices:Taking the historical price trend of Pr-Nd oxide as an example, according to SMM quotes, the average price of Pr-Nd oxide on June 30 was 444,500 yuan/mt, compared to 438,000 yuan/mt on May 30. Its average price increased by 6,500 yuan/mt in June, with a monthly increase of 1.48%. Entering July, light rare earth prices have remained stable. On July 2, the average price of Pr-Nd oxide was 444,500 yuan/mt, unchanged from June 30.

Regarding medium-heavy rare earth prices,Taking the trend of dysprosium oxide as an example, according to SMM quotes, the average price of dysprosium oxide on June 30 was 1,615 yuan/kg, compared to 1,620 yuan/kg on May 30. Its average price fell by 5 yuan/kg in June, with a monthly decrease of 0.31%. In the first two trading days of July, dysprosium oxide prices continued to remain stable at 1,615 yuan/kg.

Taking the trend of terbium oxide as an example, according to SMM quotes, the average price of terbium oxide on June 30 was 7,065 yuan/kg, compared to 7,180 yuan/kg on May 30. Its average price fell by 115 yuan/kg in June, with a monthly decrease of 1.6%. Entering July, terbium oxide prices rose slightly, reaching 7,075 yuan/kg by July 2.

Production of Pr-Nd oxide and medium-heavy rare earths increased MoM in June.

》Click to view SMM metal industry chain database

Regarding light rare earth production:

In June, Pr-Nd oxide production increased slightly MoM, with the main increase seen in Jiangxi and Shandong provinces. It is worth mentioning that the increase in Pr-Nd oxide production was mainly due to an increase in scrap recycling output. As scrap prices were favorable this month, suppliers' willingness to sell increased, and the recycling volume of scrap recycling enterprises also rose accordingly. Due to environmental protection inspections in a certain region, the production of separation plants was slightly affected in the raw ore output sector, resulting in a slight decrease in the output of Pr-Nd oxide raw materials. However, the total output of Pr-Nd oxide in June increased 2.6% MoM. [Medium-heavy rare earth production: In June, the production of Chinese medium-heavy rare earth oxides saw a slight rebound. Although the import situation for ion-adsorption ore in June was not optimistic and some separation enterprises indicated difficulties in purchasing ion-adsorption ore, most separation plants were able to maintain relatively stable production due to their raw material inventory. While the output of rare earth oxides from raw ore remained relatively stable, there was a significant increase in the output of rare earth oxides from scrap. According to scrap recycling companies, the scrap market has always been a seller's market. With an increase in NdFeB scrap prices in June, magnetic material enterprises showed a stronger willingness to sell scrap. As a result, the operating rates of most recycling companies significantly increased in June, which became the main reason for the MoM growth in the production of medium-heavy rare earth oxides. Future outlook: Based on current market feedback, most industry players, considering the downstream production cycle and order rhythm, believe that the order situation in the NdFeB industry is expected to gradually improve starting from late July. Before that, the rare earth market may continue to experience weak supply and demand: On the supply side, the onset of the rainy season in Southeast Asia leading to reduced raw material imports will provide support for rare earth prices; on the demand side, as downstream magnetic material enterprises are still in the off-season with fewer new orders, procurement is mainly just-in-time, resulting in weak demand, which will suppress rare earth prices. In summary, it is highly likely that rare earth prices will continue to fluctuate rangebound in the first half of July, with upstream and downstream players mainly bargaining within the existing price range. However, as downstream magnetic material enterprises gradually emerge from the traditional off-season, most industry players expect orders to recover in late July, driving the release of rare earth procurement demand, and rare earth prices are expected to see a phased upward opportunity by the end of July. Voices from all sides: [China Northern Rare Earth: Recent orders have maintained a steady trend, and the overall situation is better than expected. The company holds an optimistic view on future rare earth price trends] When asked about the company's expectations for future rare earth prices, China Northern Rare Earth responded during a recent institutional survey: Since Q1 2025, influenced by the tightening of upstream raw material supply and policies stimulating downstream consumption, the overall activity in the rare earth market has been better than the same period last year, providing support for the company's Q1 performance. The company seized the favorable market opportunities, focused on its annual production and operation targets, comprehensively improved the efficiency of production lines, continuously optimized the structure of raw materials and products, expanded the market in multiple ways, and deepened reforms, achieving record-high sales. In April-May, influenced by the international environment, rare earth prices experienced a brief pullback. However, as national policies gradually became clearer, attention to the rare earth industry increased, driving up product prices. Currently, the orders at the company's subsidiary, Inner Mongolia China Northern Rare Earth Magnetic Material Co., Ltd., are relatively robust, and the company holds an optimistic outlook on future rare earth price trends.

Oriental Securities believes that benefiting from the continuous optimization of the rare earth industry's supply structure, upstream smelting and processing enterprises, due to the scarcity of quotas, are expected to dominate the profit distribution within the industry chain. This will lead to controllable product quantities, mild price increases, and steady profit growth, fostering high-quality development. There exists a significant cognitive gap in the market regarding this, and it is recommended to focus on the leading groups in the global rare earth industry chain.

China Securities reported that recent U.S.-China tariff negotiations have reached a principled agreement framework, leading to a phased relaxation of rare earth export controls. Some rare earth magnetic material enterprises have obtained export licenses. NdFeB rare earth magnetic materials containing medium-heavy rare earths such as dysprosium and terbium are key materials for NEV motors. China controls approximately 70% of global rare earth ore supply, over 90% of smelting and separation capacity, and over 90% of NdFeB magnetic material capacity. Since April, magnetic material exports have declined by more than 50%, leaving overseas NEV raw material inventories critically low, with some enterprises facing production suspension risks. China's rare earth controls are not fully relaxed but only temporarily eased in the civilian sector, allowing the rare earth magnetic material sector to maintain high valuation expectations. Under the high restocking demand for overseas rare earth magnetic materials, export recovery implies a convergence of price spreads between domestic and overseas markets, with high overseas prices transmitting to the domestic market, leading to profit recovery for magnetic material enterprises. It is recommended to actively monitor investment opportunities in the rare earth magnetic material sector.